The IMF forecasts South Korea’s economy will enter a clear recovery in 2025, with growth returning to potential levels, supported by accommodative policies and structural reforms, while cautioning on external risks and calling for continued fiscal and regulatory improvements.

#YonhapInfomax #IMF #SouthKorea #GrowthForecast #StructuralReform #FiscalPolicy #Economics #FinancialMarkets #Banking #Securities #Bonds #StockMarket

https://en.infomaxai.com/news/articleView.html?idxno=92211

#IMF

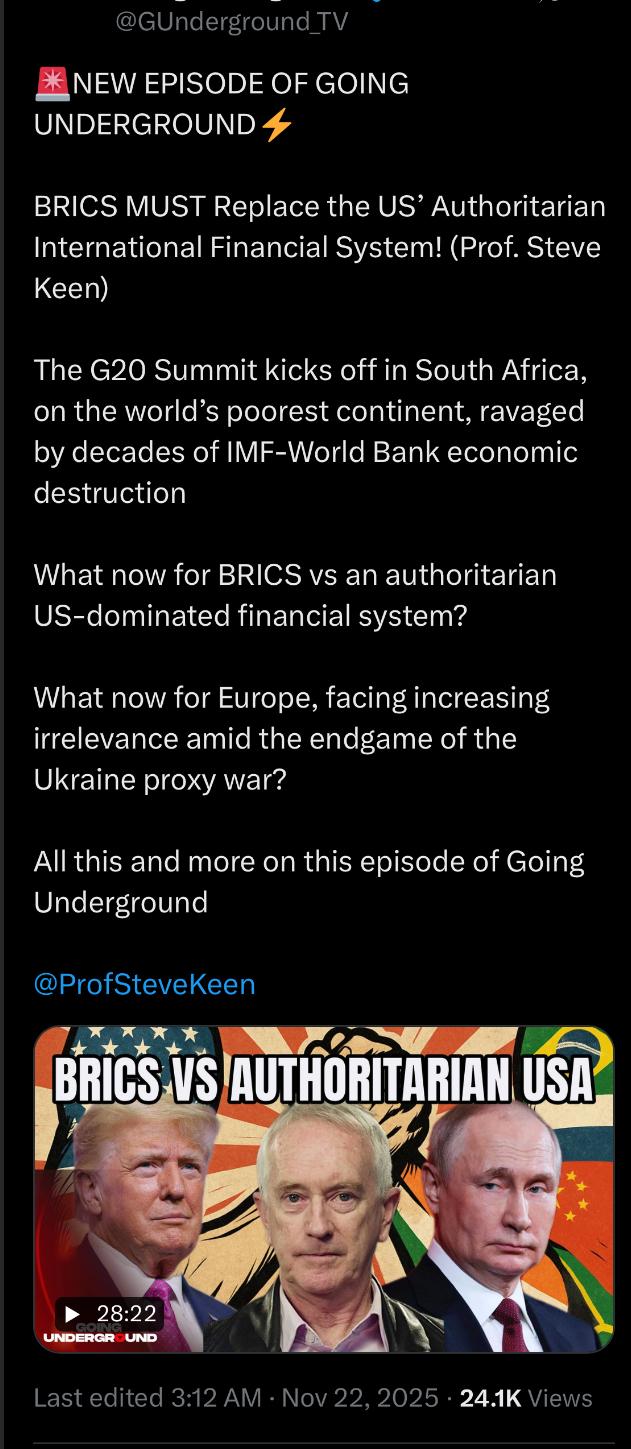

🚨NEW EPISODE OF GOING UNDERGROUND⚡️

BRICS MUST Replace the US’ Authoritarian International Financial System! (Prof. Steve Keen)

https://x.com/GUnderground_TV/status/1992144068512542848

#economy #brics #geopolitics #tiktok #international #africa #imf #china @democracy #trump #noking #europe #africa #latinamerica #cdnpoli #education #politics #usa #finance #canada #europe

IMF'den çok çarpıcı Türkiye açıklaması! Enflasyon kaça düşecek?: Uluslararası Para Fonu (IMF), 4. Madde konsültasyonu kapsamında IMF personelinin ülkeye ziyareti sonunda elde edilen ön bulguları paylaştı.

IMF'den yapılan açıklamada, yetkililerin büyümeyi korurken enflasyonu düşürme taahhüdünün önemli başarılar getirdiği, bunların enflasyonun kademeli düşüşü, liraya güvenin artması ve rezervlerin… https://www.eshahaber.com.tr/haber/?mf-den-cok-carpici-turkiye-aciklamasi-enflasyon-kaca-dusecek-273663.html&utm_source=dlvr.it&utm_medium=mastodon EshaHaber.com.tr #IMF #Türkiye #enflasyon #ekonomi #büyüme

Dünya borç batağında! Türkiye listeden kendini ayrıştırdı: 2025 itibarıyla küresel kamu borcu 111 trilyon dolara ulaştı. Bu, sadece bir yılda 8,3 trilyon dolarlık ek borç anlamına geliyor. Dünyadaki toplam kamu borcunun yarısından fazlası olan yüzde 51,8’i ABD ve Çin’e ait oluyor.

Pandemi dönemindeki zirvelerin reel olarak altına inilse de küresel borçluluk hâlâ tarihi zirvelere yakın seyrediyor.

IMF’nin… https://www.eshahaber.com.tr/haber/dunya-borc-bataginda-turkiye-listeden-kendini-ayristirdi-273522.html?utm_source=dlvr.it&utm_medium=mastodon EshaHaber.com.tr #Ekonomi #Borç #KamuBorcu #IMF #Türkiye

#america #banking #britain #capitalism #centralbank #china #corruption #currency #dollar #economics #england #empire #finance #france #gdp #gold #germany #greatbritain #history #imperialism #imf #iran #israel #japan #labor #markets #middleeast #money #nationalism #nato #netherlands #oil #policy #politics #power #russia #saudiarabia #switzerland #trade #treasury #uk #un #unitedkingdom #unitednations #unitedstates #usd #us #usa #uspol #wealth #worldbank #war

(5/6)

IMF tarih vererek duyurdu: Türkiye daha güçlü büyüyecek!: Uluslararası Para Fonu (IMF), küresel ekonomiye ilişkin son değerlendirmesinde, G20 ülkelerinin orta vadeli büyüme görünümünün 2009 küresel finans krizinden bu yana en zayıf seviyeye ilerlediğini açıkladı.

Fon, korumacılığın artması, politika belirsizlikleri, kamu maliyesindeki bozulma ve birçok gelişmiş ekonomide hızla yaşlanan nüfusun büyüme üzerinde… https://www.eshahaber.com.tr/haber/?mf-tarih-vererek-duyurdu-turkiye-daha-guclu-buyuyecek-273225.html&utm_source=dlvr.it&utm_medium=mastodon EshaHaber.com.tr #Türkiye #IMF #G20 #Ekonomi #Büyüme

Tuesday, November 18, 2025

Russia's flagship oil price drops as buyers retreat ahead of US sanctions -- Ukraine to purchase 100 Rafale jets, Zelensky says after signing defense declaration with Macron -- Russia bombed itself 8 times in 11 days, HUR intercepted call suggests -- Why Russia’s ‘super weapons’ may matter less than the Kremlin claims ...https://activitypub.writeworks.uk/2025/11/tuesday-november-18-2025/

Kansainvälinen valuuttarahasto IMF suunnittelee yhteistyötä Syyrian kanssa

⛔️⚠️IMF urges Ukraine to strengthen fight against corruption but is silent about Hungary, Slovakia, Bulgaria, and other notorious corrupt members (more) https://www.ukrinform.net/rubric-economy/4058475-imf-urges-ukraine-to-strengthen-fight-against-corruption-to-maintain-donor-support.html #Ukraine #Poland #Warsaw #Netherlands #Norway #Sweden #Estonia #Latvia #Lithuania #Paris #Rome #London #Berlin #Canada #Finland #Brussels #Denmark #Germany #France #Italy #OSCE #PACE #CoE #SouthKorea #Press #News #Taiwan #Media #Japan #US #UK #EU #NATO #UnitedStates #UnitedKingdom #EuropeanUnion #Czechia #Romania #IMF

IMF Sözcüsü Kozack'tan ABD ekonomisi için kritik uyarı! Gerilim artıyor, 4. çeyrek büyümesi beklentilerin altında kalabilir. Küresel piyasalar bu açıklamayı nasıl yorumlayacak?

Quỹ Tiền tệ Quốc tế (IMF) đã cắt giảm dự báo tăng trưởng của Mexico năm 2025 do thách thức thương mại toàn cầu. Nền kinh tế phụ thuộc vào thương mại của Mexico đang gặp khó khăn với nhu cầu giảm và chuỗi cung ứng bị gián đoạn. Doanh nghiệp cần linh hoạt để thích ứng. #IMF #KinhTeMexico #ThuongMaiToanCau https://ift.tt/YumKBwV

IMF says Senegalese government retains sovereign right to manage its debt http://newsfeed.facilit8.network/TPCJFQ #IMF #Senegal #DebtManagement #SovereignDebt #EconomicGrowth

South Korean FX experts warn that persistent low growth and the end of the US rate-cutting cycle could entrench won weakness, with the USD/KRW rate likely to remain elevated despite a current account surplus and global trade risks looming into 2026.

#YonhapInfomax #WonWeakness #USDKRW #IMF #ShinhanInvestment #GrowthForecasts #Economics #FinancialMarkets #Banking #Securities #Bonds #StockMarket

https://en.infomaxai.com/news/articleView.html?idxno=90011

“Yale University professor (#RobertShiller) born in 1946 looked to the past. His ‘cyclically adjusted price-to-earnings ratio’ is calculated by dividing a share price by the average of the past ten years of earnings adjusted for inflation. If high, the ratio warns of lower returns to say the least.

Shiller added credence to his analysis by calculating his ratio for the US #ShareMarket on a monthly basis back to 1881 – the ratio’s average over these 144 years is 17.29. At the end of October, the ratio stood at 41.20, the highest since 1881 except for when during the #DotcomBubble when it reached 44.19 in 1999.

That means the #Shiller #PEratio is higher than its 31.48 peak before the 1929 crash, when stock values plunged nearly 90 per cent. It’s almost at #DotCom heights from when the #S&P500 Index sagged 49 per cent and the tech-heavy #NasdaqCompositeIndex dived 78 per cent. Other indicators say US #stocks are more overvalued than in 2000.

Such numbers explain why so many, from the #IMF and the #BankOfEngland to even #tech #CEOs, talk of a US #StockBubble, as do #investors. A survey in October found a record 54 per cent of global fund managers (who each manage more than US$400 billion) think #ArtificialIntelligence stocks are in a bubble.”

Still questioning the AI investment bubble talk?

#finance / #prudence / #AIWinter <https://spectator.com.au/2025/11/beware-an-ai-stock-bust/>

https://www.relevante-oekonomik.com/2025/11/05/vergesst-den-internationalen-waehrungsfonds/ Vergesst den Internationalen Währungsfonds! #IMF #IWF #flassbeck

IMF mission to Senegal ends without new lending programme but talks are ongoing http://newsfeed.facilit8.network/TP7VV3 #IMF #Senegal #LendingProgram #EconomicGrowth #Finance

Africa: IMF Africa Financing a Beautiful Ugly Relationship: [New Times] The relationship between IMF financing and Africa is complex and can be described as a "beautiful ugly" one. Every time the International Monetary Fund (IMF) issues a "warning" to Africa, it lands like a concerned parent scolding a wayward child. The latest one, Africa's debt is sprawling out of control, follows the script. African governments… http://newsfeed.facilit8.network/TP72HJ #Africa #IMF #DebtCrisis #Finance #EconomicDevelopment

South Korea's Prime Minister Kim Min-seok called for swift passage of the 2025 budget, stressing the need for active fiscal policy to support economic recovery and future growth, while pledging measures to ensure fiscal sustainability.

#YonhapInfomax

#FiscalPolicy #KimMinSeok #IMF #Budget2025 #ExpenditureRestructuring

#Economics #FinancialMarkets #Banking #Securities #Bonds #StockMarket

https://en.infomaxai.com/news/articleView.html?idxno=89545

Kenya, IMF continue talks for new bailout deal http://newsfeed.facilit8.network/TP4160 #Kenya #IMF #BailoutDeal #Infrastructure #SovereignDebt

Aviation weather for Imphal airport (India) is “VEIM 040400Z 04005KT 5000 BR SCT020 BKN080 26/21 Q1014 NOSIG=” : See what it means on https://www.bigorre.org/aero/meteo/veim/en #imphalairport #airport #imphal #india #veim #imf #metar #aviation #aviationweather #avgeek vl

Client Info

Server: https://mastodon.social

Version: 2025.07

Repository: https://github.com/cyevgeniy/lmst